-

How does 2014 bode for the telecommunications sector? More specifically, what is the market outlook for technology solution vendors? On the back of rapid growth in the mobile segment, with 4G LTE take up rates increasing all over the world and the use of smart devices and consumption of rich media content becoming a lifestyle norm, the telecommunications sector is poised to continue expanding and growing. However, intense price competition, commoditization and erosion of revenues from the use of over the top (OTT) applications are impacting operator revenues. This coupled with sluggish economic growth rates across major regions in the world and saturation in the mobile market in some countries has led to the question of whether communications service providers will continue to experience bouyant growth in profits in the near term.

-

Infonetics, in its Global Telecom and Datacom Market Trends and Drivers report has outlined some points explaining the telecom and datacom market trends. Overall, capital expenditure by telecommunications service providers is expected to grow by 4%, with EMEA taking the lead despite the revenue declines experienced by operators in that region. The United States, on the other hand, is expected to ease their infrastructure capex spending for this year. The following are some key points from the report as shared by Infonetics:

-

The International Monetary Fund (IMF) anticipates the world economy will expand 3.6% in 2014 (+0.06 from 2013) amid recoveries in the UK and Germany and slowing growth in Japan, Russia, Brazil, and South Africa

-

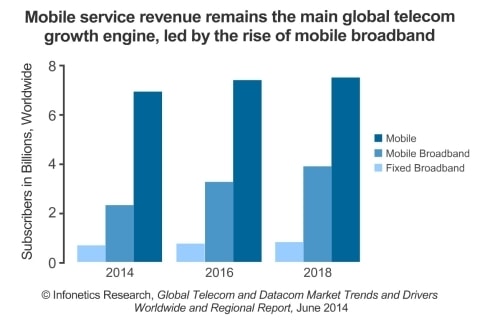

Mobile service revenue remains the main telecom/datacom growth engine worldwide, led by the unabated rise of mobile broadband

-

To avoid falling into the role of pipe provider, many service providers are deploying or weighing new architectural options such as caching/content delivery networks, distributed BRAS/BNG, next-gen central offices, distributed mini data centers, and video optimization

-

Software-defined networks (SDNs) and network functions virtualization (NFV) have the attention of nearly all service providers, who are on the long road to widespread deployments

-

Big data is becoming more manageable: Operators are leveraging subscriber and network intelligence to support marketing and loyalty strategies, churn management, and automation/optimization of networks using SDN and NFV

-

The cloud, mobility, BYOD, and virtualization are the top trends driving enterprise networking and communication technology spending, with North America leading the way

Infonetics full report is available at www.infonetics.com/contact.asp.

"Expect a slowdown in the Americas, but for a change, Europe will be in the telecom capex driver’s seat this year. We’re forecasting global carrier capex to rise 4%, with EMEA as the growth engine despite unabated low-single-digit revenue declines all across Europe. After waiting for so many years to upgrade their networks, Europe’s ‘Big 5’—Deutsche Telekom, Orange, Telecom Italia, Telefónica, and Vodafone—have decided it’s time to take the plunge.”

- Stéphane Téral, Principal Analyst for Mobile Infrastructure and Carrier Economics, Infonetics Research

“Economic expansion in mature economies and falling unemployment in Europe is driving stronger growth in enterprise telecom and datacom expenditures this year. We expect the network infrastructure segment to be the main beneficiary of growing investments, followed by security. The communication segment will likely have another challenging year, as companies evaluate their deployment strategy going forward.”

- Matthias Machowinski, Directing Analyst for Enterprise Networks, Co-Author of the Report, Infonetics Research